Every year there are new words being added to the Oxford dictionary. In March 2017 it was words like buggerlugs, sticky-outy, and Stuckism, but I wonder how long it will take until the word ‘rentvestor’ will be added?

For those who aren’t aware, ‘rentvesting’ is the concept of owning an investment property (or properties!) while renting yourself. Yes, that’s right, not everyone is after the family home before they look at purchasing an investment property.

Why would you be a rentvestor?

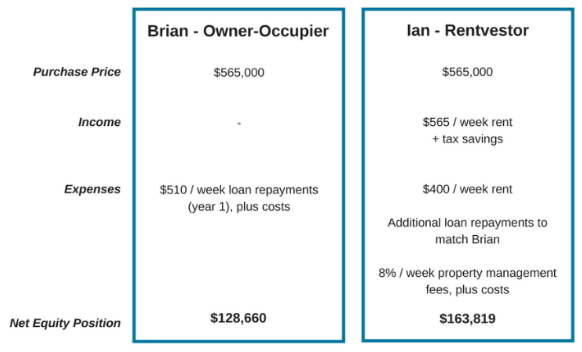

Take a look at the example of brothers Brian and Ian. Brian wants to live in his new house, while Ian is going to be rentvesting;

Brian purchases a house and land package for $565,000. He uses $137,659 to cover his deposit and costs, and has secured an interest rate of 4.2%. Brian is going to live in this house, and will be paying $510 per week to service a principle and interest loan.

If Brian kept up to date with all loan repayments and the interest rate remained at 4.2% for 6 years, adding a conservative capital growth rate of just 3% for the property and not including the deposit he already put into the property, Brian could potentially be in a net positive equity position of $128,660.

Not a bad result for Brian while keeping a roof over his head.

Ian purchases the identical house nextdoor to Brian for $565,000 also, but Ian is going to rent this one out. Ian stays in his current house where he pays $400 per week to live. His rental might not be as nice and new as the investment property he’s just purchased, but Ian is happy to live here because he’s got the bigger picture in mind with his future financial freedom.

Ian engaged Equidel prior to the purchase who ran their Equidel Property Analysis Matrix over the property, so Ian knew that the yield (or weekly rent) he could expect was going to be $565. Ian secured an interest rate of 4.7% on his loan as interest only.

Assuming a capital growth rate on the properties of 3% over the 6-year period, we can summarise this side-by-side:

So Ian our rentvestor ends up $35,153 better off than his brother Brian the owner-occupier.

Sounds like a compelling case for rentvesting, right?

But is rentvesting for everyone?

Not always. Something else you need to factor into the equation when deciding whether to rent or own is the positioning of a property for schooling and employment. Schooling is a big motivation for people to buy in certain suburbs so that they are zoned for particular schools, offering stability in education for their children. Is there really a dollar figure you can put on your children’s future and education? Knowing you will be located in a home for the next 15+ years can give you peace of mind and the opportunity to build up a sense of community in your neighbourhood. This stability is where buying over renting seems to stack up for a lot of people.

Think about the bigger picture

But for those savvy property investors who have done their homework and are working towards a better position in retirement, they may realise that renting now instead of having the dream ‘white picket fence’ may actually serve them better in the long run.

Something to keep in mind

This is only one example and the numbers are based around certain assumptions. Everyone’s individual financial situation is different, and this needs to be factored in when making any sort of investment decision. What’s right for Ian might not be right for Brian!

If you’d like to see what would work for your individual situation, give me a call. At Equidel we like to start with coffee.