If Oxford are going to be adding new phases into their dictionary this year, I believe “Social Distancing”, “Toilet Paper Apocalypse”……… and my favourite, “Quarantini”- could possibly be getting a look-in.

The start of 2020 has certainly been an interesting one. Not in our lifetime have we seen schools shutdown, borders closed, population movement restricted, and fights over toilet paper in the supermarket.

With all of this in mind, there has been much speculation in the media about the negative impact that COVID-19 will have on the Australian property market.

Speculation aside, the best predictor of the future is what has happened in the past. I’d like to take a look at some historical data, and the relevance of what we are going through today, compared to what we as Australians have overcome in years gone by.

History of Large-Scale Economic Challenges in Australia

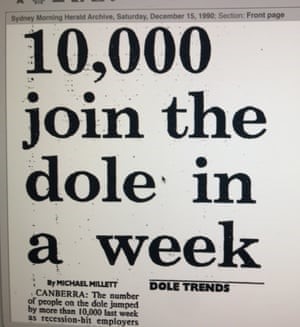

Economically we have seen challenges before. The 90’s recession – or as our PM at the time Paul Keating said: “The recession we had to have” – saw interest rates as high as 17.5% and unemployment as high as 10.8%.

Was this caused by an infection outbreak? No.

Did we shut the borders (including state borders) and restrict population movement at this time? No.

Maybe then we should look at a historical event that based on an infection outbreak….

The H1N1 Flu Virus – more commonly known as the ‘Swine Flu’ – hit Australia in early 2009, and this was most recent previous occasion that a major infection outbreak hit Australia. The Government reported 37,537 cases and 191 H1N1-related deaths. However; again in this circumstance, travelling restrictions were not in place, and our borders remained open.

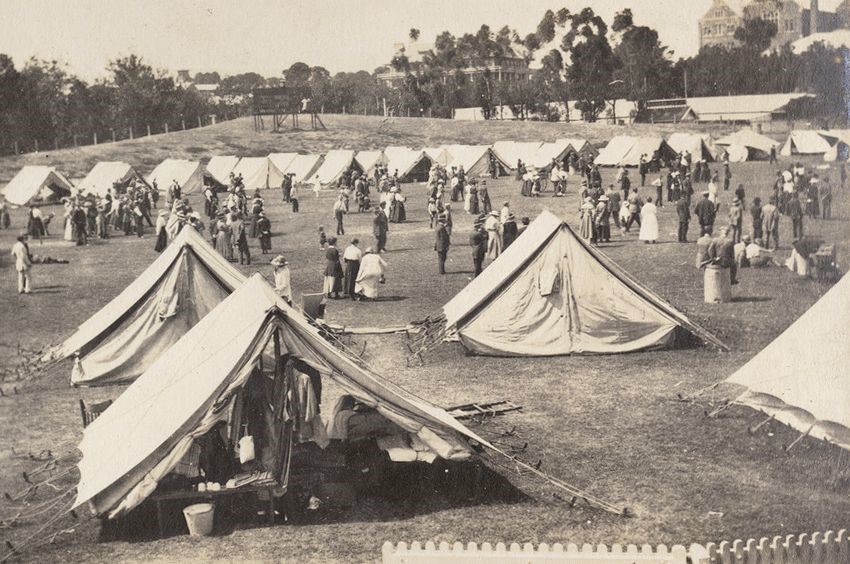

The last time we experienced border restrictions was actually just over 100 years ago when the Spanish Flu hit Australia in 1919. It was reported that around 40% of Australians were affected by the Spanish Flu, with somewhere between 13,000 to 15,000 Australians losing their lives (multiple sources report different figures). This was shortly after the end of World War 1 and the population in Australia at the time was approximately 5,000,000 people.

But 1919 was a vastly different time in Australia. We know that Australia now has over 5 times that population figure, and that the forecast for future population growth is far greater than the global current average. We may need to look towards more recent history to gauge the potential effects that COVID-19 may have on the property market.

More Recent Economic Challenges

From mid-2007 to early 2009, the world experienced the GFC or Global Financial Crisis. There were a multitude of factors which were the cause of the GFC and according to RBA, there is still debate over “the relative importance of each factor”.

This crisis was not brought about by a pandemic, but more so by irresponsible lending (compared to current policies) by “Subprime Borrowers” which flooded the market with risky loans in the United States. These loans were approved without the lenders closely assessing the borrower’s ability to make loan repayments and were based around the “widespread presumption that favourable conditions would continue” (RBA).

Australia did not experience the downturn which the US experienced through the GFC due to the banks having very little exposure to the US housing market, and also due to very little Subprime lending in Australia, thanks to the historical lending standards by APRA (Australian Prudential Regulatory Authority).

So how is the GFC relevant to COVID-19? While borders didn’t shut, we did see unemployment increase.

The question then remains, can unemployment effect the performance of the property market?

Can unemployment effect the performance of the property market?

History indicates that there has been strong growth in some property markets which have high unemployment compared to the national average.

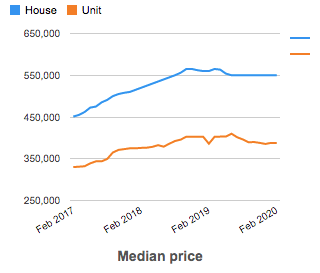

Let’s use Tarneit in Victoria as an example. With an unemployment rate of 8.1% in 2016, some could say that the potential for growth in the property market may have been grim. However; over the last 10 years, the Tarneit property market has performed (grown) with a more than respectable annual rate of 5.39% per annum.

(Source: YourInvestmentPropertyMag.com.au)

In the last census, Aroona in Queensland also had a higher than national average unemployment rate of 7.3% (Australia at the time was 5.6%) however; Aroona’s property market has continued to grow with an average over the last 10 years of a respectable 3.39% pa, and 4.61% in the last 12 months. (RP Data)

So how have these areas continued to grow, and how will COVID-19 impact these property markets in the future?

Population growth.

Population growth has been a huge factor in the continual growth of Tarneit and other property markets, and because this is currently restricted due to COVID-19 due to border closures, this is probably the one factor that will have the largest negative impact on the property market.

IS IT ALL DOOM AND GLOOM?!?!

The media will have you believe that it is. I’d like to refer you back to our previous blog: Yes, the property boom is over. But where?

In this piece we touched on the negative and outrageously false predictions by economic experts with relation to property markets around Australia.

To be fair, I do see some value in these predictions. For example, if we plan for the worst and it doesn’t eventuate, we are only in a better position than we otherwise would have been if the experts were more accurate. But I don’t believe in media sensationalism for the sake of getting a few clicks.

Anyway, back to the point – high unemployment, borders shut, decrease in property listings, and so much uncertainty.

How can the property market not be facing strong decreases?

Unlike the “Recession we had to have”, interest rates are at an all-time low and currently only 1 in 12 home loans are experiencing 6 months of grace from monthly repayments.

This could potentially prevent some 8.3% of the current property market owners from defaulting on their loans, and thus prevent an influx of “must sell” properties coming onto the Australian property market.

Combine this with an overall decrease in property listings (4.9% decrease from March 2020 to April 2020), and we could see a decrease in property supply across the board.

Adding to this, the ABS reports in March 2020 show a -2.5% change in residential investor lending compared to the previous month. This means that there are likely to be less property investors in the market, competing for the same properties, and also potentially preventing over-supply in investment stock in certain markets.

Is now the time to invest in property?

In summary, while there is an obvious decrease in population growth, we are also seeing:

- less properties available on the market due to people holding off listing their properties (supply),

- a halt on distressed selling of already owned properties due to the halt in loan repayments by the banks (supply),

- an all-time low interest rate bringing first homeowners and bargain hunters into the market (demand), and

- a decrease in investors preventing an over balance of rental stock in some property markets.

Thankfully we are now starting to see restrictions slowly easing across Australia, positive news that a possible COVID-19 treatment is already going through clinical trials, and the even better news that Australia and New Zealand are looking at an international travel agreement between both countries!

While a possible treatment for COVID-19 might be months away and even longer for a vaccine, what I am more interested in is the fact that Australia is now looking at how we can open our borders, and to who will we be opening them up to.

How far away really are we from an increase in population growth??

The one piece of advice I give to property investors…….. make sure you are ready!!